As per the Black’s Law Dictionary, to “Compound” means to settle a matter by a money payment, in lieu of other liability.” Thus, Compounding is a mechanism that provides the offender an opportunity to avoid prosecution for an offence committed by him by way of a monitory payment in lieu of it. It is the process of voluntary acceptance of contraventions and seeking redressal for the same by avoiding a long drawn process of prosecution. It helps in minimising both cost and time and enables the person in default to make honourable discharge of his/her liability.

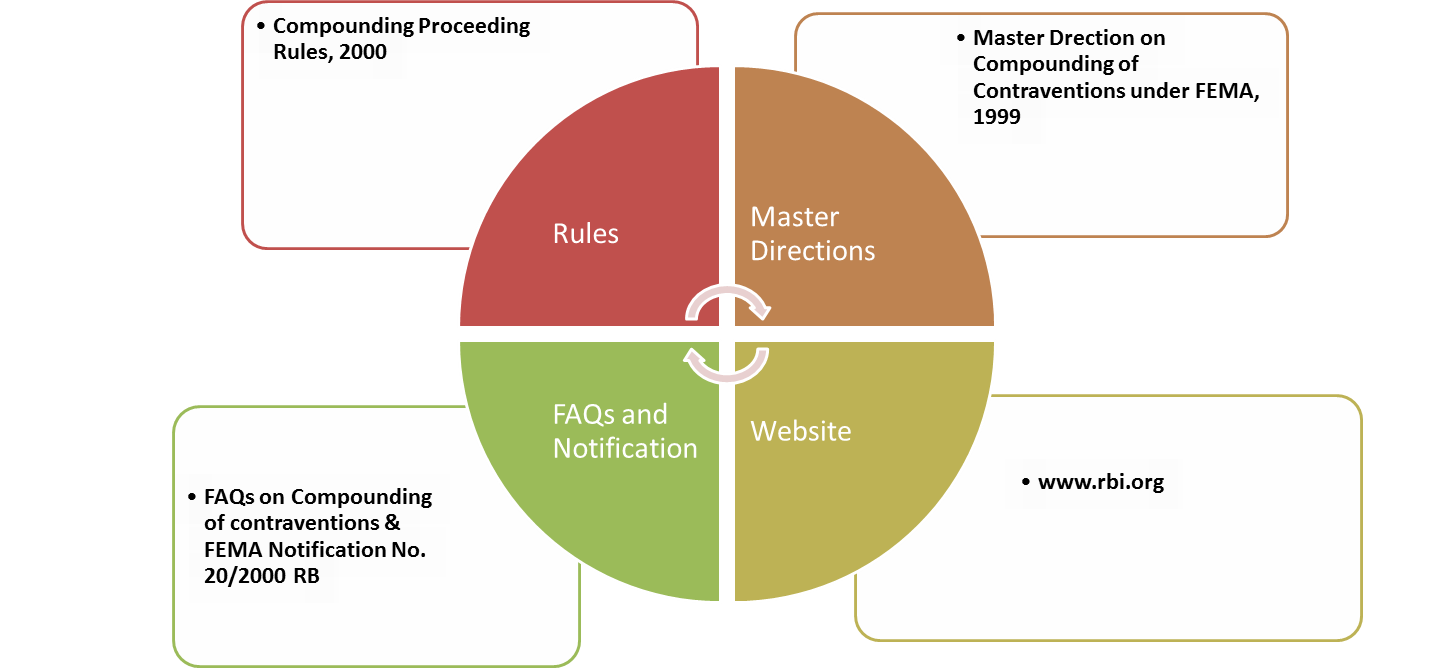

The attention of the reader is sought to the below figure, that depicts the Legal Framework for Compounding of Offenes under FEMA in India.

Willful, malafide and fraudulent transactions, serious contravention suspected of money laundering, terror financing or affecting sovereignty and integrity of the nation are, however, viewed seriously, which will not be compounded by the Reserve Bank.

Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking redressal.

The following are the benefits of admitting a fault, pleading guilty and seeking redressal via Compounding Mechanism:-

A contravention can be suo- moto admitted and disclosed to the RBI by a party at fault or the RBI can initiate further action on becoming aware of the said contravention by any of the following means:

The Government of India has in consultation with the Reserve Bank placed the responsibilities of administering compounding cases to the Reserve Bank of India except in case of serious contraventions i.e Hawala Transactions. The compounding with respect to Hawala Transactions shall be reffered to the Enforcement Directorate.

Contravention is a breach of the provisions of the Foreign Exchange Management Act (FEMA), 1999 and rules/ regulations/ orders/ circulars issued there under. The RBI can compound any contravention under FEMA on receipt of a specified sum and after offering an opportunity of personal hearing to the contravener. However, in the case of Hawala Transactions, the compounding authority lies with the Enforcement Directorate.

The RBI before passing a Compounding order, considers various factors for arriving on the compounding amount to enable the contravener to make an honourable discharge of his/her liability:

The compounding amount to be payable by the contravener is calculated by the RBI on the basis of certain parameters mentioned above and on the basis of the RBI Guidance Structure for the same. It may, however, be noted that the guidance note is meant only for the purpose of broadly indicating the basis on which the amount to be imposed is derived by the compounding authorities in Reserve Bank of India. The actual amount imposed may sometimes vary, depending on the circumstances of the case taking into account the factors indicated in the foregoing paragraph. The reader can have a detailed look at Compounding of Contraventions under FEMA, 1999. And RBI Master Directions with respect to the same.

Since, compounding is a voluntary process, there is: No provision of appeals against the order of the Compounding Authority; No Request for reduction of amount compounded; No Request for extension of time for payment of amount imposed.

The RBI also provides for a simple procedure for payment of late fees to regularise the instances of delay in reporting under FEMA. Please visit Late Submission Fees( LSF) for details.

You may also like to read about the Procedure to be followed for making a Compounding Application.

I have one query. In the case of DI filing, whether the same has to be done by investor Company or investee company.

A foreign entity holds 100% stake in an Indian Company under FDI norms. Now if that Indian Company (XYZ Limited) has invested 100% in another Indian Company(PQR Limited), whether DI filing has to be done by XYZ or PQR.

Pursuant to Rule 23 Foreign Exchange Management (Non-Debt Instrument) Rules, 2019 read with Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019 an Indian Company making downstream investment (i.e. investor company) in other Indian entity (i.e. investee company) (which is considered as indirect foreign investment) is required to file Form DI with Reserve Bank of India within 30 days from the date of allotment of equity instruments.

Hence, as per the rules investor company is liable to file Form DI.

However, due to practical challenges faced in FIRMS portal and as per the format of Form DI, it is Investee Company who files Form DI with the Reserve Bank of India as the portal automatically updates the shareholding pattern of the Company filing the form which results in increase in the paid up share capital of the Company (which means if investor company would file the form, the investment would become a part of its paid up share capital).

Therefore, in case downstream investment, the investee company files the Form DI and the investor company is responsible to ensure the timely filing of Form DI and other compliances with the provisions of aforesaid rules.

In your case, XYZ Limited is responsible for filing Form DI, however the same shall be filed with business user of PQR Limited.