All of us are aware that many counties have entered into double taxation avoidance agreement (“tax treaties” or “DTAA”) with other countries to mitigate the problem of double taxation which reduces the tax liability of residents of one treaty country in other treaty country i.e. by avoiding double taxation of same income in both the countries.

In cases where no tax treaty is in place, the income may be taxed in the home country (basis tax residency) as well as in the source country (where income is earned) leading to double taxation of the same income. Many cases have been reported where a person acting through a legal entity has obtained treaty benefits “improperly” by forming layers of entities which would not be available to such person directly. This is generally done in case of passive income i.e. Dividend, Royalty or Interest Income. Let us understand this with the help of an example:

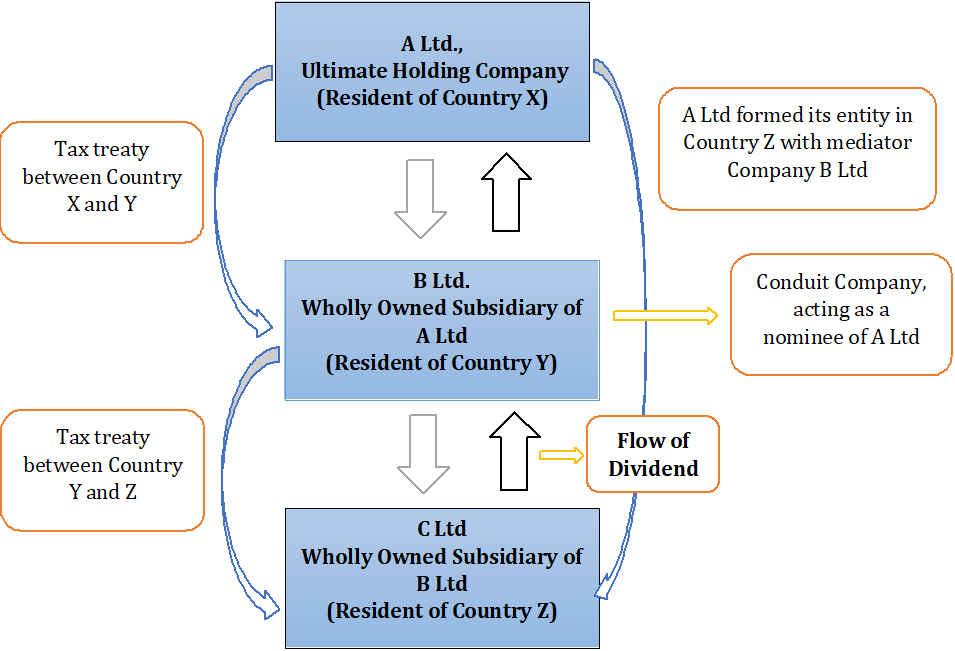

In the above example, A Ltd. is the resident of Country X and wants to target the market of Country Z for business expansion and growth. However, Country X and Country Z do not have a double taxation avoidance agreement which would lead to double taxation of same income in both the countries. Hence, A Ltd forms a wholly owned subsidiary company in Country Z with the help of a intermediate/ conduit company B Ltd of Country Y which has a double taxation avoidance agreement with both the Countries X and Z.

The profits earned by C Ltd are delivered to B Ltd by way of dividend and B Ltd in turns distributing the dividend to A Ltd. Hence, in this way, A Ltd has reduced its tax liability (which it would be liable to pay if it had directly invested in C Ltd) by availing the benefit of tax treaty entered between the Country Y and Country Z.

The entities who acts as a medium for channelizing income from other sources are termed as “Conduit Company”. In the given case, B Ltd is a conduit company.

The term “Beneficial Owner” is nowhere explicitly defined under the Income Tax Act and in the tax treaties. However this term is being used significantly under various provisions and is considered as a benchmark to test whether the beneficial provisions of tax treaty should be provided to tax payers.

However, under civil and common law and as explained by Organisation for Economic Co-operation and Development (OECD), beneficial owner for the purpose of tax treaty, is a person who is the ultimate beneficiary of income and also has a control over it i.e. a person who receives the income for its own use.

You can visit our other blogs on Rights and Obligations of a Beneficial Owner and Transfer of Beneficial Interest in Shares to develop a better understand on the topic “Beneficial Owner”.

The Government of India has emphasized on word “beneficial owner” in double taxation avoidance agreements (DTAA) entered with various countries for providing treaty benefits implying its intent to provide tax benefits only to beneficial owner only.

This regime acts on the principle of agent or nominee relationship. An agent or a nominee receiving any income on behalf of his principal are not provided any exemption or relief, since they are acting as a mediator to channelize the income from other sources and are not the actual owners of the income. Hence, it may be interpreted as inconsistent with the intent of law to provide them relief only due to their status of residency. Fundamentally, the tax treaty aims to provide benefit to those only who are the ultimate owners of the income by reducing their tax burden.

Likewise, conduit companies may also be considered as having only acted as an intermediary for the parent company as they may be held as not having beneficial interest and accordingly exemption or relief provided under tax treaties may not be available to it. Let’s understand the same through below decided cases:

There have been many instances domestically as well as internationally where the Companies have availed the benefit of tax treaties by forming chain of complex corporate structures. Some of the case laws are listed below:

| Sr. No. | Name | Facts of the Case | Issue and Judicial Pronouncement |

| 1. | Prevost Car Inc. v. The Queen |

|

Concerning Issue: Dutch Co. was not entitled to avail benefit of tax treaty entered between Canada and Netherlands as it was not a beneficial owner of Dividend, since it was acting as a conduit of UK and Sweden Co. The Court found the case in favour of Prevest Car, concluding that the Dutcho Co. owned the shares on its own and is entitled to receive dividend on the share and hence, it shall be considered as a property of Dutch Co. The Court considered the ownership of Dutch Co. and held that it was the beneficial owner of Dividend and is eligible to avail benefit of tax treaty. Thus, in this case, even a conduit company i.e. Dutch Co. was considered as “beneficial owner” and the benefits of tax treaty available to it was not denied inspite of its status of being a wholly-owned subsidiary. |

| 2. | HSBC Bank (Mauritius) Ltd. vs. Deputy Commissioner of Income-tax (IT)-2(2)(2), Mumbai |

|

Concerning Issue: The Company claimed exemption from Indian taxes on interest income. However, the exemption was denied by the tax authorities on the ground that the Company was not meeting the conditions prescribed under the tax treaty to claim such exemption. The Company filed an appeal to the Mumbai Bench of the Income Tax Appellate Tribunal (“the tribunal) against the order of tax authorities. The Company drew attention of tribunal on the Circular No. 789/2000 dated 13th April, 2000 issued by the Central Board of Direct Taxes which prescribes that Tax Residence Certificate issued by the Mauritian authorities will constitute as a valid evidence of beneficial ownership and the same was ruled by the Hon’ble Bombay High Court in case of DIT v. Universal International Music B.V. The tribunal considered the aforesaid circular and relied upon the judgment issued by the Bombay High Court and also the Chennai Bench in case of Hyundai Motor India Ltd. v. Dy. CIT, held that the Company was the beneficial owner of interest income and is eligible to claim exemption. |

| 3. | KSPG Netherlands Holding B.V. Vs. Director of Income Tax |

|

The tax authority stated that since the companies are required to deduct Dividend Distribution Tax (DDT) on payment of dividend, it is not taxable in the hands of shareholders. Therefore, if Pieburg India has paid the DDT to the tax authorities, dividend would not be taxable in India in the hands of receiver i.e. KSPG or the ultimate holding company. Further, as per the India-Netherland treaty, tax on capital gains cannot be levied and collected by Indian Tax Authorities. However, the questions were raised on the beneficial ownership of such gain. It was contemplated that since the German Company was ultimate holder, India-Germany treaty would be applicable. The authority desisted to give a ruling and envisaged that merely by its holding a Company cannot be termed as “Conduit Company” as both the entities have its own legal entity. Hence, for the time being, unless the transfer actually takes place, it was considered that the KPSG is not liable to pay tax on capital gains. |

In the light of aforementioned rulings, it can be observed that judgement of courts are truly based on the facts of cases since there is no clarity what would construe as beneficial owner.

In the example given above, where B Ltd is acting as a conduit for A Ltd and re-distributing the dividend received from C Ltd. to A Ltd. would be eligible to claim benefits of tax treaty if we rely on the judgment in case of Prevost Car Inc. Vs. The Queen provided B Ltd is able to prove itself before tax authorities as being beneficial owner and not just working as a conduit company. However, the same can vary depending on the circumstances and facts of the case.

Considering the above, one can truly understand the essence of provisions related to beneficial owner only when proper law would be enacted by the Government under taxation laws or definition is included in DTAA. The law would certainly bring more clarity and transparency.