A foreign entity can sell to Indian consumers through internet without having to establish a physical place of business in India. They can also register under GST laws.

India has the second largest number of internet users in the world and India also being one of the fastest growing large economies, the business potential on internet related services is tremendous. Though there have been consistent efforts by the Government of India to bring transparency and ease of doing business in India, there are sometimes apprehensions by non-residents before committing huge investments in the country by a complete setup. With use of internet, the same may not be essential in all cases as a consumer in India can be a recipient online (through internet) without having any physical interface with the supplier of such services from outside India.

In this digitalized era, if a non-resident or foreign entity is targeting Indian consumers through internet, and is carrying a business in India requiring mandatory registration under Goods and Service Tax (GST) Law of India or if such entity is voluntarily desirous of obtaining the same for future business in India, can get itself registered under GST Laws through the online services for registration provided by the Indian Government. It shall be allotted a GSTIN, which is15 digit PAN based unique Identification Number for doing business in India.

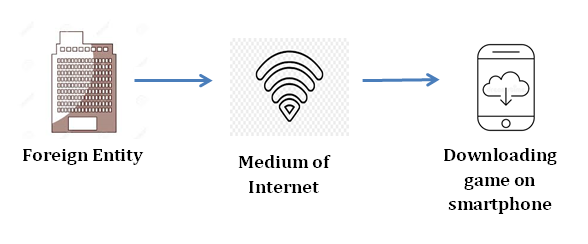

GST for Non-Residents is a wide subject but here we will focus on applicability on provision of service by a non-resident entity through the medium of internet, to end consumers in India. It is pivotal to understand as to which online transactions are covered under the ambit of GST. Let us take an example to understand this better: Mr. A, an Indian boy downloaded an e-game (manufactured by XYZ, a USA entity) through the Android Playstore on his mobile phone.

In the above example, the foreign entity based outside the territory of India is supplying services of selling games online via medium of internet to consumer in India. Now, it would be impractical to ask the recipient in India (Mr. A, in our case) to register and undertake the necessary compliances under GST for a one-off purchase on the internet. Thus, understanding the practical difficulty, the supplier of services (XYZ) getting business from India even though located in a non-taxable territory outside India, shall be the person liable for paying integrated tax on such supply of services.

Therefore, the supplier of services located in a non-taxable territory shall apply for GST Registration in India for providing such services.

Now, a question arises that whether every online transaction shall be triggered for taxation under GST. The answer is NO. The IGST Act, 2017 has specifically categorized the services whose delivery is mediated by information technology over the internet or an electronic network and the nature of which renders their supply essentially automated, involving minimal human intervention and impossible to ensure in the absence of information technology. Such services are distinctively categorized under the IGST Act, 2017 under the concept of Online Information Database Access and Retrieval services (hereinafter referred to as OIDAR).

OIDAR is a category of services provided through the medium of internet and received by the recipient online without having any physical interface with the supplier of such services.

The above services includes electronic services such as,

Hence, only the above stated list of services involving medium of internet shall raise the liability of paying GST.

A Non- Resident OIDAR services provider is covered under the categories of person requiring compulsory registration under Section 24(xi) of Central Goods & Service Tax Act, 2017 (CGST Act) in India .

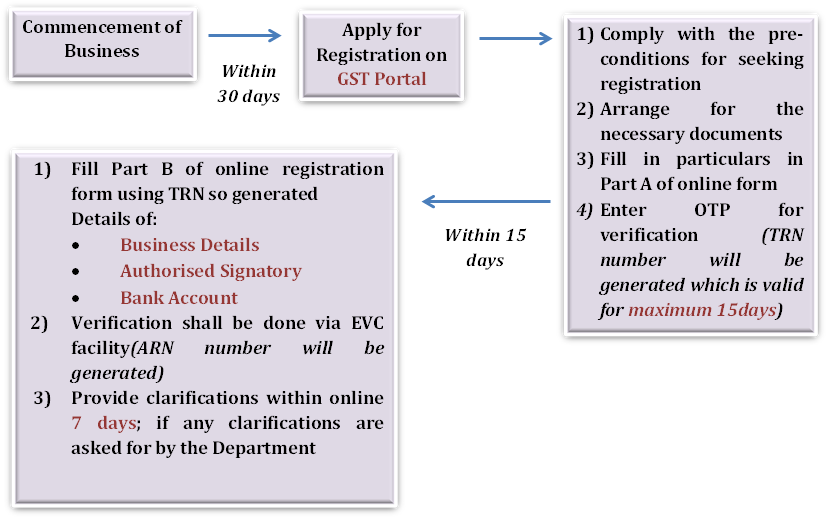

The GST Registration shall be taken within 30 days of commencement of business.

Note: No pre-deposit of advance tax shall be required in case of Non- Resident OIDAR services provider.

Penalty: 100% of tax due or Rs. 10,000, whichever is higher

The online mode for GST registration brings out two methods of applying for such registration:

Case 1: XYZ does not have/ does not desire to have a presence in India

In this case XYZ is required to appoint an individual as Authorised Signatory which can be resident in India or a non-resident, who shall apply for registration on behalf of XYZ.

The liability for paying integrated tax under GST and complying with necessary GST provisions remains on the Non- Resident entity itself.

Note: As per CGST Act, 2017 PAN is mandatory for seeking registration under GST. But for ease of business for Non- Resident OIDAR services provider who do not have any presence in India, the requirement of PAN has been relaxed i.e PAN is optional for such Authorised Signatory.

Case 2: XYZ has/ is desirous of having a presence in India

In this case XYZ is required to appoint in addition to an Authorised Signatory (as explained above) an Authorised Representative which has to be a resident (whether individual or a corporation) in India holding a valid PAN, who shall apply for registration on behalf of XYZ.

The liability for paying integrated tax under GST and complying with necessary GST provisions shifts to the Authorised Representative.

A Non-Resident Online Services Provider must fulfill following conditions so that they can register on the GST Portal:

It is appreciable to note that laws are in place to facilitate GST registration online for those companies which do not have physical presence in India. However, it is relevant to note the applicability of the Companies Act, 2013 to such a company. As per foreign companies definition under companies Act, 2013, a company or a body corporate registered outside India and having engaged in business through electronic mode is covered under the definition of a foreign company (Sec 2(42) of the Companies Act, 2013). Since, it is a foreign company, it needs to comply with the provisions applicable to it under Chapter XXII of the Companies Act (Sec 379 of the CA 2013). The Government has to come out with clear laws easing out the compliances rather than entangling the businesses with multifarious regulations.