Updated by Pooja Dhiman and Janvi Gupta as on October 29, 2020

Indian chartered accountants are known worldwide for their higher understanding and financial skills. Prime Minister Narendra Modi had once referred chartered accountants as “big pillar” of the Indian economy and their services to the nation are deeply valued.

Pursuant to the provision of Section 141 (1) of the Companies Act, 2013 a person or a firm shall be eligible for appointment as an auditor of a company only if he is a chartered accountant or majority of partners of the firm is a chartered accountant and practising in India. We have summarised here as few aspects relating to appointment of auditor, tenure, filling up casual vacancy, rotation etc.:

1.1 I have just incorporated a Company, when do I need to appoint the first Auditor of the Company and how?

The First Auditor shall be appointed by the Board within a period of 30 days from the date of registration (incorporation) of Company. E-form ADT-1 is required to be filed within 15 days from the date of appointment.

Note: The governing law, the Companies Act, 2013 (the “Act”) nowhere specifies that the first Auditor shall be appointed at the first Board Meeting of the Company, it only mandates to appoint the Auditor within 30 days from the incorporation. Having said this, in general practice the first Auditor is appointed at the first Board Meeting.

1.2 What if the Board is not able to appoint the first Auditor within 30 days of incorporation?

If the Board fails to appoint such Auditor, then it shall inform the members of the Company about the same. The members shall within a period of 90 days from date of incorporation, at an extraordinary general meeting, appoint the first Auditor of the Company.

1.3. What would be the tenure of office of the first Auditor?

The first Auditor, appointed as above, shall hold the office till the conclusion of the first Annual General Meeting of the Company.

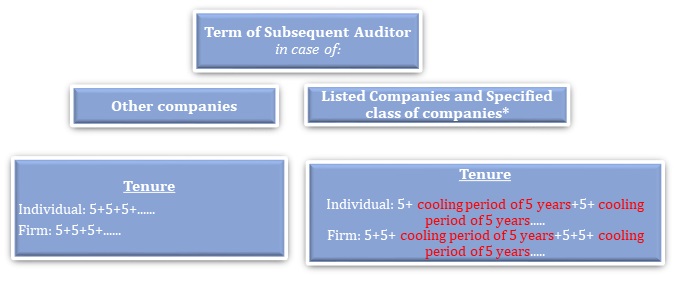

2.1 What is the term of appointment of subsequent Auditor under Companies Act, 2013?

The subsequent Auditor i.e. appointed after the completion of tenure of first Auditor at the first Annual General Meeting of the Company, shall hold the office from the conclusion of the first Annual General Meeting till the conclusion of sixth Annual General Meeting and thereafter till the conclusion of every sixth meeting, so on and so forth.

However, as per Section 139(2), certain Companies cannot continue with the same auditor after expiry of one term (in case of individual) or two terms (in case of firm) of five years. We have illustrated the concept as follows:

Please note that one person companies and small companies are excluded from the above category.

2.2 What is the term of appointment of Auditor for specified class companies under the Companies Act, 2013?

The subsequent Auditor i.e. appointed after the first Auditor for specified class of companies shall hold the office:

Individual: For one term of 5 years and then a cooling period of 5 years is to be provided i.e. can be re-appointed after a break of 5 years.

Firm: For two terms of 5 years i.e. 10 years and then a cooling period of 5 years is to be provided i.e. can be re-appointed after a break of 5 years.

2.3 Can the Auditor be appointed for a period less than 5 years?

The terms for appointment of Statutory Auditors is defined under Section 139(1), which clearly stipulates that the auditor appointed shall hold office till the conclusion of sixth AGM from the AGM in which he is appointed. Thus, one can opine that the auditor cannot be appointed for one term, consisting of period less than or more than five years. Even if a Company has previously appointed an auditor for a term lesser than 5 years, it shall still be treated as one full term and the cooling period under Section 139(2) shall be required for specified companies.

If the auditor is appointed to fill in the casual vacancy arisen due to vacancy of office of previous years, then, the period he serves to complete the tenure of the previous auditor (i.e. till the conclusion of ensuing AGM) shall not be counted as term of this auditor and he can be appointed for a fresh term of 5 consecutive years in the same Company.

2.4 Is e-form ADT-3 required to be filed after completion of the tenure of the Auditor?

The purpose of e-form ADT-3 is to intimate the ROC about the termination of the office as a result of resignation of the Auditor before the expiry of his/her tenure. The Auditor who has resigned, is required to file e-form ADT-3 within a period of 30 days from the date of resignation. Thus, e- form ADT-3 is not required in following situations:

3.1 What can be the possible instances when the casual vacancy arises?

Casual Vacancy is vacancy in the office of auditor before the expiry of the tenure for which he was appointed to that office. The grounds of casual vacancy can be resignation, death or disqualification of the Auditor (this is an inclusive list).

3.2 What is the manner of appointment of new auditor, if casual vacancy of the auditor arises in the Company?

| Sl No. | ||

| Resignation of the Auditor | Other than the resignation of the Auditor | |

| 1 |

Casual Vacancy to be filled by the Board within a period of 30 days. This appointment is subject to the approval of shareholders of the Company. |

To be filled by the Board within a period of 30 days. |

| 2 |

The appointment to be the approved by the members (in EGM or AGM, as the case may be) within a period of 3 months from the date of appointment. |

No member’s approval is required. |

| 3 |

The Auditor who has resigned, is required to file e-form ADT-3 within a period of 30 days from the date of resignation. |

No e-form ADT-3 is required to be filed. |

| 4 |

E-form ADT-1, towards appointment, is required to be filed within 15 days from the date of appointment, i.e. General Meeting at which the appointment recommended by the Board, is confirmed by the members of the Company. |

E-form ADT-1, towards appointment, is required to be filed within 15 days from the date of appointment, i.e. Board meeting held to fill casual vacancy. |

3.3 What would be tenure of auditor appointed in casual vacancy?

Auditor appointed for filling the casual vacancy shall hold the office till the conclusion of the ensuing Annual General Meeting.

3.4 Whether the form filing is required at every type of appointment of auditor?

Yes, for every type of appointment i.e. first auditor, casual vacancy or re-appointment at AGM, the Company shall file e- form ADT-1 for such appointment. In case the retiring auditor is reappointed, the Company shall report the prior period served by the auditor in Form ADT-1.

3.5 Is Form ADT-3 is required to be filed in case of the death of an Auditor?

No, e-form ADT-3 is not required to be filed in case of the death of an Auditor.

4.1 Is the concept of rotation of auditor applicable to every company?

No, the provisions pertaining to ‘Rotation of Auditors’ are applicable only on to the specified companies as mentioned under earlier in this article.

4.2 As of what date should the limits as applicable on specified class of companies be reckoned for rotation of an auditor i.e. whether it should be checked at the beginning of financial year or during the financial year or any other such date?

The law specifies no date at which such limits should be reckoned (say end of financial year/ audit of accounts/ during the year, etc.) Thus, one must be prudent and follow conservative approach. Further, as soon as the concept of rotation of auditor becomes applicable on the Company i.e. the Company crosses the threshold limit as specified in the Act during the tenure of an auditor, that auditor will continue his office till the conclusion of AGM of the Company until which he was appointed (per previous term), however, thereafter he shall not be re-appointed in the same Company until 5 years. A new auditor shall be appointed by the Company at the AGM at which the tenure of the existing auditor expires/ is completed.

5.1 The tenure of the retiring auditor is over and he is eligible for reappointment, however, the Company does not want to appoint him. Is there any special provision for this?

If the one term of the auditor is completed, it is the Company’s wish whether or not to reappoint the retiring auditor. Per the Act, subject to Section 139(1) and the rules made thereunder, a retiring auditor may be re-appointed at an annual general meeting, if—

5.2 What if no resolution was successfully passed at AGM to appoint or reappoint an auditor?

Where at any annual general meeting, no auditor is appointed or re-appointed, the existing auditor shall continue to be the auditor of the company.

6.1 We have appointed the Auditor of the company for a term of 5 years. However, some differences have crept in and we want to remove the existing Auditor? He is not resigning, nor giving audit report, what to do?

The mechanism for removal of a Statutory Auditor of the Company before expiry of the term appointed under the Act has been provided under section 140 of the Act read with Rule 7 of Companies (Accounts and Audit) Rules, 2014.

File application in e-form ADT-2 along with the grounds of removal and other details, for Central Government approval (at present, the powers have been delegated to the jurisdictional Regional Director) within 30 days of the resolution passed by the Board.

Special resolution to be passed by the members of the Company at the general meeting, to be held within 60 days of receipt of approval of the Central Government.

The term of the auditors came to an end in the AGM. However,no new auditor was appointed.As per Section 139(10) the existing auditor will continue.My queries:

What will be the term of appointment of the existing auditor ?

Will a resolution be passed in the same AGM wherein his term ended or an EGM be conducted for the same ?

Will a written consent also be required ?

Other than ADT-1 what additional forms will be required in this regard.

Dear Reader,

Please note, pursuant to Section 139(10) of Companies Act 2013, if no auditor is appointed or re-appointed at the annual general meeting, the existing auditor will continue to act as an auditor and shall continue in their role until a new auditor is appointed.

Further, since appointment of auditor is a specific item in the agenda of annual general meeting, passing of resolution is necessary. A resolution for the continuation of the existing auditor can be passed in the same AGM where his term ended. It doesn’t necessarily require an EGM unless the company’s articles of association provide for same.

Also, as per Explanation to Section 139(1), appointment includes re-appointment. Therefore, before re-appointment of an auditor, a written consent from the existing auditor is required for his continuation in office.

Besides filing Form ADT-1 for the appointment of auditors, no additional specific forms are required for the continuation of the existing auditor. However, the company needs to ensure that necessary resolutions and consents are properly recorded and maintained in compliance with the Companies Act 2013 and Companies (Audit and Auditor) Rules, 2014.

in case of OPC one auditor firm was appointed for 5 years till FY 2025-26. Signing was done by partner who changed his CA firm subsequently . what is to be done to continue that CA (now partner with new CA firm) as a auditor.

Will it be considered as casual vacancy ?

Dear Reader,

As per our understanding company wishes to replace their current auditor’s firm with new auditor’s firm with existing partner before the current auditor’s tenure is expired.

Companies Act, 2013 allows for dismissal or replacement of auditor under section 140(1) of the Companies act 2013. Company can remove its auditor appointed under Section 139 from his office before the expiry of his term only by passing special resolution and obtaining other necessary approval prescribed under the Companies Act.

Further, Casual vacancy is not defined under the act and in general context it may arise out of death, disqualification, resignation or removal etc. of the auditor or non-ratification of appointment by the shareholders.

Pursuant to provision of Section 139(8) of the Companies act 2013, any casual vacancy in the office of the auditor shall be filled by the Board of Directors within thirty days For further assistance in this regard, you may seek professional advice in this matter.

Hello,

Facts of the case:

-Our’s is a private Company with the borrowing of more than 50crs and this threshold has exceeded on 31st March 2023

– The audit firm is appointed for every one year instead of Five Years

– The audit firm is auditor of company from more than 5years

Question:

– As the firm is appointed for less than 1year, is it considered as 1 term?

-further the threshold has crossed during the tenure of the Auditor, so will this term be considered as completing one term under the provision of Section 139(2)

-So, If it is considered as 1 term, does that mean the firm is eligible for appointment for only term?

– While re appointing, do we also need to consider that firm is appointed as auditor from the past five years?

Dear Reader,

Thank you for approaching us. Based on the facts stated by you, we understand that the provisions pertaining to rotation of auditor are applicable on the Company as on 31st March, 2023 (due to total borrowing exceeding INR 50 crores). Further, the Company is contemplating re-appointment of the existing auditor.

However, to guide you on the further course of action, we will require a more comprehensive analysis of additional facts and the relevant documents. Therefore, you may connect with us for professional assistance in the aforementioned matter.

Respected Sir,

I request you to provide your valuable guidance on below matter;

In private company, an auditor has just resigned 3 days before AGM for which ADT- 3 is filed with roc.

Before AGM , Company will not be able to get consent and eligibility from proposed new auditor so in AGM what to do? How to appoint auditor in casual vacancy?

Dear Reader,

According to section 139 sub-section 8 of Companies Act, 2013, any casual vacancy in the office of an auditor shall be filled by the Board of Directors within thirty days, but if such casual vacancy is as a result of the resignation of an auditor, such appointment shall also be approved by the company at a general meeting convened within three months of the recommendation of the Board and E-form ADT-1, towards appointment, is required to be filed within 15 days from the date of appointment.

On the basis of facts shared by you, we suggest that during the AGM you may inform the shareholders about the resignation of the previous auditor and the resultant casual vacancy. Seek shareholder approval in the AGM to appoint the proposed auditor (even if you have not obtained their consent and eligibility yet).

Once the AGM is concluded, promptly obtain the written consent and eligibility certificate from the newly appointed auditor and file other required documents.

A Company fall under prescribed class of company. It has appointed a auditor firm for 1st term for a period of 1 year (2017-2018) and reappointed for 2nd term for a period of 5 years (2018-23) can they be reappointed further for a period of 4 years?

Dear Reader,

Pursuant to section 139 (1) and (2) (b) of the Companies Act, 2013, Companies as may be prescribed shall not appoint/reappoint an audit firm as auditor for more than two terms of five consecutive years.

Therefore in accordance with this provision it is to be noted that the appointment or reappointment is done for a fixed term which should not be more that 5 consecutive years, even if a company had previously hired an auditor for a period less than five years, it is still considered one complete term.

Hence, the auditor who has completed two terms of his appointment cannot be reappointed for further period after completion of tenure of its second term unless cooling period of 5 years mentioned in proviso to section 139 (2) is completed. We assume that the Auditor so appointed was not the first auditor of the Company.

A company appointed a firm for 5 years, during the tenure of the firm, one partner sign the Financial Statements (FS) for 3 years and another partner sign the FS for 2 years.

Q Can another partner sign the FS or first partners sign the FS for 5 years?

Q. Can Company reappoints the firm for next 5 years?

Q. Can a third partner sign the FS for next 5 years?

Q. Can same partners sign the FS for next 5 years?

Dear Reader,

Please find below our response to your queries.

Question-1: Can another partner sign the FS or first partners sign the FS for 5 years?

As per the provisions of Section 22 of Partnership Act 1932- In order to bind a firm, an act or instrument done or executed by a partner or other person on behalf of the firm shall be done or executed in the firm-name, or in any other manner expressing or implying an intention to bind the firm.

Further, there are no provisions under the Companies Act, 2013 restricting the above-mentioned manner of signing. Therefore, per our view, any partner of the firm may sign the financial statement of the company within the period of their tenure.

Question-2: Can Company reappoints the firm for next 5 years?

As per Section 139(2) of Companies Act 2013, read with Companies (Audit and Auditors) Rules, 2014-

No listed company or the company belonging to such class or classes of companies as may be prescribed shall appoint or reappoint:

an individual as auditor for more than one term of five consecutive years; and

an audit firm as auditor for more than two terms of five consecutive years:

Therefore, if the company does not fall into the above-mentioned category, or even if it does, the auditor has completed only their first term, the Company is eligible to proceed with the re-appointment of the firm for the subsequent five years.

Question-3: Can a third partner sign the FS for next 5 years?

As per the above quoted provisions, a firm can be appointed for the two terms of five consecutive years and any partner can sign the financial statements on behalf of the firm in the said tenure.

Question-4: Can same partners sign the FS for next 5 years?

In absence of any restrictive provisions, we are of the view that same partner can sign the financial statements for the next 5 years.

Rule 5(c) refers to public borrowings exceeding Rs 50 cr for applicabilty of rotation of auditors to unlisted Companies. Whether the borrowings referred to are sanctioned limts or actual availed limits? And if actual availed limts ,what is the date of applicability for rotation of auditors

Dear Reader,

As per Section 139(2) of the Companies Act, 2013 (“the Act”) read with the Rule 5(c) of the Companies (Audit and Auditors) Rules, 2014, one of the criteria of applicability of rotation of auditors to unlisted companies is if the Company has outstanding loans or borrowings from banks or public financial institutions in excess of fifty crores. However, the provisions of the Act are silent on the whether such limits are to be considered on sanctioned basis or actual basis. Based on the practice followed, it should be considered on actual basis.

Regarding the applicability of rotational of auditor on the Company, we suggest that it should be checked at the time of appointment or re-appointment of auditor due to the following reasons:

1. Since the appointment or re-appointment of statutory auditors is done for a fixed term which should not be of more than 5 consecutive years and the provisions of the Act does not mention for appointment for any specified years;

2. After reading the language of Section 139(2) of the Act, it is clear that it should be checked at the time of appointment or re-appointment; and

3. In case the existing term of the auditor is not yet complete, then there is no case of appointment or reappointment. Hence, it is only when the existing term is complete that the question of rotation will arise.

For further assistance in this regard, you may connect us to seek professional advice in this matter.

If you feel that we have been able to address your query, kindly review us on Google.

In case auditor form has complete two tenure in the company and the company hasn’t appointed the auditor in the AGM. Will it be termed as Casual Vacancy?

As per section 138(10) if a company has not appointed or reappointed the auditor in AGM, the existing auditor shall continue as the auditor of the company. will it be applicable in my case, where auditor has complete two terms?

In case it is not casual vacancy, what procedure i should follow for the compliance of law for appointment?

Dear Reader,

The term “Casual Vacancy” has not been defined under the Companies Act, 2013 (“the Act”). However, Casual vacancy may arise in case of death, disqualification, resignation or removal etc. of the auditor.

Based on the facts provided by you, the same shall not be considered as casual vacancy but a case of rotation of auditors.

Further, pursuant to Section 139(2) of the Act read with Rule 5 of the Companies (Audit and Auditor) Rules, 2014 (“the Rules”), no listed company or such class of Companies as specified in the rules, shall appoint or re-appoint an auditor firm who has completed 2 terms of 5 consecutive years.

In case the aforesaid provisions are applicable on the company, the existing auditor firm shall be ineligible for further appointment and in that case, the Company shall be required to appoint a new auditor or audit firm. As per section 139 (10), the existing auditor shall continue to hold office till the appointment of new auditor. But this enabling provision of section 139 (10) shall not be construed as a deviation from the law and the company shall not take a view that the existing auditor shall perpetually continue till next AGM. This matter also deserves same level of urgency and attention as in the case of appointment in casual vacancy. You may explore to appoint a new auditor at the earliest in a duly convened EGM.

For further assistance in this regard, you may seek professional advice in this matter.

Where this clarification regarding fresh term of 5 years is written in act in case of casual vacancy ,any circular specifically mention that reappointment of auditor wiil be considered as fresh appointment

Dear Reader,

There is no specific circular that has been issued by the Ministry for clarifying the term of auditor in case of casual vacancy.

However, we would like to bring to your kind notice the following provisions pertaining to appointment of auditor:

a) Section 139(1) of the Companies Act, 2013: states that every company shall, at the first annual general meeting (AGM), appoint an individual or a firm as an auditor who shall hold office from the conclusion of that meeting till the conclusion of its sixth annual general meeting and thereafter till the conclusion of every sixth meeting.

b) Section 139(8) of the Companies Act, 2013: provides that the auditor appointed to fill the casual vacancy shall hold the office till the conclusion of the ensuing AGM.

After completion of the term of casual vacancy, the Company has an option to choose whether to continue with the same auditor by seeking approval of shareholders at the AGM. Such appointment, if approved by the shareholders, shall be made under Section 139(1) and shall be of a fixed term of five years.

Thus, as per our interpretation of aforesaid provisions the appointment under Section 139(8) is different from appointment under Section 139(1), and accordingly does not fall under Section 139(2) for reckoning of transitional period.

a private limited company crosses the threshold limit of 50 crores in Borrowings in FY 2022-2023. Statutory Auditor was appointed for 5years from 2020-2025.(FROM incorporation he is continuing as Auditor)

Whether Company has to appoint new Auditor after completion of his term in 2025 or in the AGM TO BE HELD IN 2023?

Dear Reader,

Even if the borrowings of a private company exceed INR 50 crores in the year 2022-23 which falls within the tenure of the existing auditor i.e., 2020-21 to 2024-25, the existing auditor can continue to hold office and complete his tenure as sub-section (1) Section 139 states that an auditor shall hold office from a period of 5 years from the date of his appointment.

However, in the AGM that will be held for the FY 2025 in which the tenure of the existing auditor will be coming to an end, the Company will need to appoint a new auditor and the existing auditor cannot be re-appointed as per the sub-section (2) of Section 139.

Dear Sir,

Members of the company had appointed the “Firm” of CAs (firm having 2 CAs as partners) as Auditor of the company, however during the year one of Partner CA lefts the firm and firm gets dissolved as Only one partner remains in the firm.

In the records of the ICAI, same FRN continuous in the name of New Proprietorship concern as it was in firm’s name.

In the Given Situation, whether the Company is required to appoint new auditor considering the dissolution as the casual vacancy in the office of the auditor ?? or Auditor should tender his resignation and then company should fill the casual vacancy of the auditor??

Dear Reader,

The term casual vacancy is not defined under the Companies Act, 2013. However, in general parlance, it means a vacancy in the office of an auditor due to resignation, death, removal, or any other reason resulting in the incapability of the auditor to perform duty.

In our opinion, the dissolution of the partnership firm would result in a casual vacancy in the office of the auditor. Thus, there would be no requirement to obtain the resignation of previous auditors (i.e., partnership firm) as the dissolution of the partnership firm has itself resulted in a casual vacancy.

The Board of Directors of the Company pursuant to the power vested to them under Section 139(8) can appoint a new auditor (i.e., sole proprietor firm) after obtaining their consent and eligibility letter, and will be required to file Form ADT-1 with the Ministry to report such appointment.

A Private limited Company has exceeded borrowings of 50crore in FY 2022-2023. However existing Auditor was appointed on 2020 for 5 years till 2024-2025.(He is the statutory Auditor from incorporation).

Should the Company appoint new Auditor after completion of his term in 2025 or in the AGM to be held in 2023?

Dear Reader,

Even if the borrowings of a private company exceed INR 50 crores in the year 2022-23 which falls within the tenure of the existing auditor i.e., 2020-21 to 2024-25, the existing auditor can continue to hold office and complete his tenure as sub-section (1) Section 139 states that an auditor shall hold office from a period of 5 years from the date of his appointment.

However, in the AGM that will be held for the FY 2025 in which the tenure of the existing auditor coming to an end, the Company will need to appoint a new auditor and the existing auditor cannot be re-appointed as per the sub-section (2) of Section 139.

Therefore, the company can appoint a new auditor after the completion of his term in FY 2025.

But in subject case, if as on 31.3.2025 i.e. in the b/s of 31.3.2025 FY 24-2025, if borrowings is less then Rs. 50 crores, then what will be the case? can we continue the retiring auditor for further term of five years? – i think the criteria shall be required to be checked at the time of appointment / re-appointment.

your views pl sir.

Dear Reader,

As per the provisions of Section 139(2) of Companies Act 2013, the concept of “Rotation of Auditor” shall apply to the following class of companies excluding one person companies and small companies:

(a) all listed companies.

(b) all unlisted public companies having paid up share capital of Rupees ten crore or more;

(c) all private limited companies having paid up share capital of Rupees fifty crore or more;

(d) all companies having paid up share capital of below threshold limit mentioned in (a) and (b) above, but having public borrowings from financial institutions, banks or public deposits of Rupees fifty crores or more.

In the absence of any contrary provisions, it is our understanding that the threshold shall be determined based on the financial statements of the previous financial year at the time of appointment or re-appointment.

Therefore, if the company is having paid up share capital below than the threshold mentioned in (a) and (b) above and if the borrowings is less than 50 crores in the previous Financial Year, it can re-appoint the same auditor as the company no longer falls among the classes of company mentioned in Section 139(2).

We have appointed an audit firm as Statutory Auditor in FY 2019 for period of 5 years, whose term is expiring in FY 2023. We are Pvt Ltd company having paid up capital of INR 9.6cr and borrowings less than 50cr

Before 2019 also, we had same firm as Statutory Auditor.

Can we continue with same auditor or do we need to change in this Pre-Agm ?

Can I appoint them on yearly basis as per old Companies Act or 5 years term is must ?

Dear Reader,

As per rule 5 of the Companies (Audit and Auditors) Rules, 2014, following classes of companies shall not appoint or reappoint an individual as auditor for more than one term of five consecutive years or an audit firm as auditor for more than two terms of five consecutive years:

a) all unlisted public companies having paid up share capital of rupees ten crore or more;

b) all private limited companies having paid up share capital of rupees fifty crore or more;

c) all companies having paid up share capital of below threshold limit mentioned in (a) and (b) above, but having public borrowings from financial institutions, banks or public deposits of rupees fifty crores or more.

As your company is a private company having paid up share capital of INR 9.6 crore (which is less than the threshold limit mentioned in clause (b) above) and borrowings less than the threshold limit as mentioned in clause (c) above, therefore the company can continue to appoint the previous auditor.

Further, your company cannot appoint an auditor on a yearly basis as section 139(1) strictly stipulates that the auditor appointed shall hold office till the conclusion of sixth AGM from the AGM in which he is appointed i.e., for a period of 5 years from the date of his appointment in AGM.

Sub : Appointment of Auditor

A Private Company appointed XYZ as Statutory Auditor for 5 years. The Company has borrowings of more than Rs.50 Crore. The 5 years term ended in 2020. The Company has appointed new Statutory Auditor ABC for another 5 years. After completion of 1 year, ABC do not want to continue and willing to resign. Can the Private Company appoint XYZ for another 5 years.

Dear Reader,

Based on the information shared by you, we believe that auditors namely XYZ and ABC are audit firms. If so, according to the provision of Section 139 of the Companies Act, 2013 an audit firm can be appointed as auditor for more than two terms of five consecutive years. Since XYZ has already served its one term of 5 years, they are eligible to serve for further 5 consecutive years.

However, if the auditor so appointed is an individual, XYZ will not be eligible to be appointed for another period until completion of a cooling off period of five years from the date of demitting the office of the statutory auditor, as the company falls under the class of companies under Rule 5 of the Companies (Audit and Auditors) Rules, 2014.

in a Private company auditor not filing ITR and Annual return for the FY – 2020-21 & 2021-22 what is the remedies available for the company

Thanks

Dear Reader,

Please note that it is not the duty of the Auditor to file ITRs of the company. You may still file ITR for FY 2021-22. However, for the FY 2020-21, you shall apply for condonation of delay under section 119 2(b) of Income Tax Act, 1961.

can statutory auditors i.e audit firm can be appointed for less than 5 years?

Dear Reader,

The terms for appointment of Statutory Auditors is defined under Section 139(1), which clearly stipulates that the auditor appointed shall hold office till the conclusion of sixth AGM from the AGM in which he is appointed. Thus, one can opine that the auditor cannot be appointed for one term, consisting of period less than five years.

In case of private company if auditor was appointed by casual vacancy for 1 year and then approved in EMm but in the AGM for subsequent term another auditor is appointed ,then does ADT-3 needs to filed by auditor who was appointed in casual vacancy ?

Dear Reader,

Pursuant to the provision of Section 139 of the Companies Act, 2013, the Board shall fill the casual vacancy of a statutory auditor, and the same shall be approved by the shareholders in their meeting within three months from the date of the board’s recommendation and hold the office till the conclusion of the next AGM.

Further, regarding the filing of ADT-3, Section 140(2) prescribes the requirement of filing the said form within 30 days from the date of resignation.

In case of a Listed Co., can a retiring statutory auditor become the internal auditor of the same Company during his cooling period?

Dear Reader,

Please note that the Companies Act, 2013 places no restriction on an Individual / Firm being appointed as Internal Auditors after the completion of rotation period for statutory auditors which is 5 years or 10 years as the case may be. The relevant provisions of the Companies Act are silent on that aspect.

Hence, we can conclude that the statutory auditor appears to be eligible to be appointed as Internal Auditor for the same company.

However, the guidance note issued by ICAI on Independence of Auditors state that the Auditor or the firm should avoid any situation in the near future, which may be interpreted as threat to his/their independence, for example, acceptance of assignment related to internal audit and management consultancy services within one year of completion of assignment.

Our company is Unlisted Public Company. In 2017, while appointing the auditor, rotation of auditor was applicable. Now the 2 terms of existing Auditor is coming to end in coming AGM. But now the rotation of auditor section is not applicable to company as it does not fall into the criteria of classes of companies. Can we appoint same auditor for another 5 years?

Dear Reader,

The Companies Act provides for rotation of auditors for such classes of Companies as prescribed under section 139(2) read with rule 5 of the Companies (Audit and Auditors) Rules, 2014.

Further, the first proviso to section 139 (2) provides that the auditor who has completed his term under section 139 (2) shall not be eligible for re-appointment as auditor in the same Company for five years from completion of his term.

According to our interpretation of the foregoing requirements, the Company can re-appoint the auditor because the Company no longer falls among the classes of companies to which the provisions of section 139(2) apply. Hence, the first proviso to section 139 (2) which places limitation on eligibility for re-appointment on auditors who have completed their terms in the same Company, does not apply to it.

We are a Private company and does not fall under provisions of section 139(2). We have a separate branch auditor for branches in India other than the Statutory auditor. Should the appointment of branch auditor be also for a period of 5years and do we have to file Form ADT 1 for the same?

Dear Reader,

Please note, section 143(8) of the Companies Act 2013 provides that a branch auditor of a company shall be the Company’s Auditor,i.e, the Statutory Auditor of the company or a person who is qualified to be appointed as an auditor under this Act and appointed as such under section 139 of the Companies Act 2013.

Hence, based on the above provision of law, we can deduce that all requirements under section 139 of the Companies Act 2013, shall be suo motto applicable to a Branch Auditor as well, including the provisions relating to the prescribed period of appointment of 5 years subject to the liberty of the company for any further re-appointment and intimation of the said appointment in form ADT-1 with MCA. However, the same is to be read keeping in mind the provisions of section 143(8) of the Companies Act 2013 and Rule 12 of the Companies (Audit and Auditors) Rules 2014.

How much gap can be there in appointment of another internal auditor after resignation of previous internal auditor? and tell me the consequences of not appointing internal auditor within time.

Please note that there is no specific provision in Section 138 of the Companies Act, 2013 (“the Act”), regulating the time period for the appointment of new internal auditor in the event of the resignation of the incumbent auditor. The board, however, must fill the vacancy at the next board meeting following the resignation and file e-form MGT-14 with the Registrar.

In the case of non-compliance with Section 138 of the Act, the aforementioned clause does not contain any specific penalties. Therefore, the penal provisions of section 450 of the Act will apply, and the company and every officer of the company who is in default or such other person will be liable to a penalty of INR 10,000, plus a further penalty of INR 1,000 for each day during which the contravention continues, up to a maximum of INR 2,00,000 in the case of a company and INR 50,000 in the case of an officer who is in default.

Hi,

Is it necessary that at the time of recommendation of appointment of Auditor by Board (in case of casual vacancy), the Board must have the consent and certificate from the Proposed Auditor? Can it be obtained after Board meeting but before notice of EGM??

Dear Reader,

As per the proviso to Section 139(1) of the Companies Act, 2013, every company is required to obtain from the auditor being appointed a written consent and certificate of eligibility before his appointment.

In case of a casual vacancy, the board will pass a resolution for recommending such an appointment to the members, to substantiate this; the board must obtain the consent and certificate of eligibility from the proposed auditor.

Thus, given the above provisions, we can infer that it is necessary to obtain consent and a certificate of eligibility from the proposed auditor before the date of the board meeting being held for recommending the appointment of the proposed auditor.

The audit firm was the branch auditor of a company. After a period of 2 years the firm was also appointed as a auditors of the HO. The period of rotation will be counted from the audit of branch audit or HO audit ?

The provisions of Section 143(8) of the Companies Act, 2013, states that the accounts of the branch office shall be audited either by the auditor appointed for the Company (i.e., head office) or by any other person qualified for appointment as an auditor of the company under this Act and appointed as such under section 139.

Therefore, it can be inferred that the Act does not restrict the appointment of the same person as a statutory auditor in the branch and the head office. Accordingly, the tenure of 5/10 years shall be calculated considering the period of his office as a statutory auditor in the branch and head office (since the head office and branch office falls under the same company). However, if separate auditors have been appointed for the branch and head office, the tenure of both the auditors shall be counted separately.

Thus, in our view, taking into consideration the intent of the law and to maintain the integrity of the audit process, the period of rotation shall be counted from the date of appointment in the branch office.

Can subsequent auditor be appointed for 1 year ??

As per Section 139(1), a Statutory Auditor shall hold office from the conclusion of the first AGM till the conclusion of the sixth AGM. Thus, one can opine that the auditor cannot be appointed for one term of the auditor cannot be less than or more than five years. Hence, subsequent Auditors shall not be appointed for 1 year.

Ratification of Auditor: the provision w.r.t Annual ratification of Auditor has been omitted Companies Amendment Act, 2017 read with notification S.O. 1833E dated 07th May, 2018

What is the remedy or consequences of appointing Subsequent Auditor for a period of 1 year(till the conclusion of next AGM) in private limited company for FY 22-23? ADT-1 has also been filed for this specifying appointment of subsequent auditor for 1 year

Dear Reader,

An auditor shall be appointed for a term of 5 years. Section 139(1) of the Companies Act, 2013 (the “Act”) strictly stipulates that the auditor appointed shall hold office till the conclusion of sixth AGM from the AGM in which he is appointed i.e., for a period of 5 years from the date of his appointment in AGM.

Since your private company has appointed a subsequent auditor for a period of 1 year, it has contravened the provisions of Section 139 for which penal provisions have been provided in Section 147 (1) of the Act.

For contravention of any of the provisions of Section 139, the company shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees and every officer of the company who is in default shall be punishable with fine which shall not be less than ten thousand rupees but which may extend to one lakh rupees.

For further assistance, you may contact us to seek professional advice in this matter.

Dear Sir,

An unlisted public co. Borrowings crosses 50Cr as on 31st Mar,2019.Paid up capital is below the limits prescribed. An Audit firm was serving as auditor for past 10 years and is reappointed for another term of in AGM held in 2019. Kindly clarify the below issues:

1. Are the limits prescribed in Rule 5 of the Companies (Audit and Auditors) Rules,2014 to be checked “At “ the time of appointment of audit firm?

2. For the calculation of term specified in section 139(2), the period served as an auditor before the applicability of limits specified in Rule 5, be counted?

Thank you in Advance.

A CA who is releaving from existing partnership and forming new partneship with new partners. The existing company audited by him are not liable for rotation under 139(2). But while filing ADT 1 we filed for a term of 5 years in name of our old partnership. whether the new partnership entity can become next auditor by filing a fresh ADT1. whether recovation is possible since we filed ADT 1 for five years with our FRN number of old firm. what can we do in this scenario

Dear Sir,

This seems to be a case of dissolution of an Audit firm wherein a new firm is being formed with new partners. It would result in Casual Vacancy due to reasons other than Resignation. In such a situation, the Company may take note of such dissolution and appoint the new firm in its Board Meeting (after obtaining consent from the new audit firm) and file a fresh Form ADT 1 with the Ministry mentioning the details of the new audit firm. It is advisable to attach a clarification letter in the Form explaining the formation of a new firm with the new composition of partners.

Hello sir

an auditor is appointed in case of casual vacancy will hold office till ensuing agm.

now my query is whether in that ensuing agm company have to file adt1 again to appoint the auditor (which was appointed at the time of casual vacancy) for 5 yrs or the form which was filled at the time of casual vacancy (ie.adt1) will be sufficient

The third proviso of Section 139 (1) states that “the company shall inform the auditor concerned of his or its appointment, and also file a notice of such appointment with the Registrar within fifteen days of the meeting in which the auditor is appointed”. Also, explanation to this proviso states that “appointment” includes reappointment.”

Since the auditor is being reappointed, the company shall be required to file Form ADT-1 with the Registrar.

Hello Sir,

We appointed sole proprietorship firm as our auditor for 5 years in our 2 companies. In one company their tenure is expiring this year but in another company their tenure will expire next year. Now that sole proprietorship firm has been changed to partnership firm. Please guide what compliance we need to do.

Pursuant to Rule 6(3)(ii) of the Companies(Audit and Auditors) Rules, 2014 for the purpose of the rotation of auditors, the incoming auditor or audit firm shall not be eligible for appointment if such auditor or audit firm is associated with the outgoing auditor or audit firm under the same network of audit firms. Here “same network” includes the firms operating or functioning, hitherto or in the future, under the same brand name, trade name, or common control.

Therefore, the outgoing sole proprietorship firm had completed one term of 5 consecutive years and if such firm converts itself into a partnership firm, such converted partnership firm cannot be appointed as auditor for the same companies as they are under the same control.

Also, as per Rule 5 of The Companies (Audit and Auditors) Rules, 2014 the rotation of auditor is applicable to the following class of companies:

An auditor is appointed for 5 years of a private limited company vide ADT-1. Before the tenure of 5 years ends, the board wants to appoint a new auditor in the ensuing AGM. What are the implications and compliances to be followed wrt documentation & form filings?

Pursuant to Section 140(1) of the Companies Act, 2013 (‘the Act’) read with Rule 7 of the Companies (Audit and Auditors) Rules, 2014 an auditor appointed under section 139 of the Act may be removed from his office before the expiry of his term only by way of a special resolution of the company subject to the prior approval of the Central Government.

Further note an opportunity of being heard shall be given to the concerned auditor before taking any action for removal.

In this regard following compliance needs to be done:

Can Individual Auditor and Partner of Firm be reappointed (without break of 5 years)for further period of 5 years in Pvt. Ltd. having share capital less than 50 Cr.

The provisions related to the rotation of statutory auditors do not apply to private companies having paid-up share capital of less than INR 50 crore or having public borrowings from financial institutions, banks or public deposits of less than INR 50 crore. Further, small companies are exempt from the provisions of Section 139(2). Kindly refer to Section 139 and Rule 5 of The Companies (Audit and Auditors) Rules, 2014.

very good query and answer session

my question is that RD-1 is invalid reflacted on MCA 21 portal but ADT-2 is approved. what I shoud do.

The details provided are not sufficient to answer the query. Request you to provide us a brief background on your query.

Whether ADT-1 filing mandatory for every fives years in the case of pvt ltd companies not falling under Sec 139(2).

Pursuant to the provision of Section 139(1) of the Companies Act, 2013 read with Rule 4 of the Companies (Audit and Auditors) Rules, 2014 a statutory auditor will be appointed in an AGM for a period of consecutive 5 years who will hold the office till the conclusion of every sixth AGM from the date of appointment. The notice of such appointment is made to the concerned RoC in form ADT-1 within 15 days from the date of appointment/re-appointment.

Therefore, every company has to file form ADT-1 for the appointment of an auditor once the period of 5 years gets completed irrespective of whether the company is falling under section 139(2) of the Companies Act, 2013.

sir,

a company appointed auditor firm for five years. But after completing 2 years, the auditor firm dissolved. as the firm dissolved, the auditor cannot file ADT-3. Whether the dissolution of auditors firm can be treated as disqualification? so that board can appoint new auditors ?

Pursuant to the provisions of Section 141 of the Companies Act, 2013, the dissolution of the firm cannot be qualified as a disqualification, however, the non-existence of an entity does create a casual vacancy in the office of the auditors.

Further, pursuant to the provisions of Section 140(2), form ADT-3 is required only in the case where the auditor has resigned himself, which is not the instance in your case. Therefore, being a casual vacancy, the Board can appoint the new auditors subject to the approval of shareholders and thereafter file form ADT-1.

Our company has mistaken appointed a new auditor in case of casual vacancy for 5 years instead of reappointment. Is this Form ADT-1 valid? Are there any consequences? Please tell me the procedure to rectify it.

Your question is not clear, nonetheless from this query we understand that in case of casual vacancy, the auditor was appointed for 5 years (ideally, the auditor filling the casual vacancy should have been appointed till the next AGM only and then either the existing auditor/ new auditor should have been re-appointed/ appointed, as the case maybe, at the AGM for next 5 years).

Assuming that the SRN for Form ADT-1 has been approved, please note that in this case the Company has to approach its jurisdictional ROC for getting the SRN cancelled, and thereafter the Company can pass a new resolution in the suppression of earlier resolution and can file a new Form with appropriate data thereon.

If an auditor is appointed as auditor for those companies in which rotation of audit is not falling then what to fill in ADT-1 “Specify the tenure of previous appointment(s) of the auditor or auditor’s firm or its member in the same company in

which audit was conducted or is functioning (excluding previous years having break of five or more years as specified

in Rule 6)

Number of financial year(s)”

The very purpose of point 4(i) in form ADT-1, is that the company filing the form provides the details of the earlier engagement(s) of the auditor(s) being appointed/ re-appointed with that of the company.

So, if the auditor has been appointed for the first time in a company on which provisions of Section 139(2) is not applicable, you can insert “0 Years” and proceed. Further, in the case of reappointment of statutory auditor whether it is a firm or the partner of the firm, details of their prior engagement with the company should reflect in the form.

Dear sir I have a query. We had appointed an audit firm ABC ltd for a tenure of 5 years but before the completion of the tenure, say after 2 years that firm merged with another firm xyz ltd. Now we have to appoint xyz ltd as our new auditor. While filing ADT-1 what should we mention in point 4(i) in form ADT-1? New firm has common partners and section 139(2) is not applicable to us.

In the given case, the Company needs to provide the details of previous office of auditor held by ABC Ltd. in point 4(i) of the Form ADT 1.

In a listed company, which is under IBC, what happens if shareholders donot approve appointment of Auditors appointed by COC at next AGM ? Will the auditors have to be changed or COC can reappoint them ?

According to the provisions of the Companies Act, 2013, appointment of every auditor is required to be approved by the members in the annual general meeting.

Further, Section 28(1)(m) of the Insolvency and Bankruptcy Code, 2016, the Resolution Professional is required to take prior approval of the Committee of Creditors (COC) to make any changes in the appointment or terms of contract of statutory auditors or of the corporate debtor.

Accordingly, in view of the provisions of IBC and Companies Act, 2013, the provisions doesn’t specify w.r.t. disapproval by members to appoint auditors in the general meeting. Therefore, where the members have denied the approval of auditors in the general meeting, COC cannot appoint the same auditors and new auditors are required to be appointed subject to approval of members in the general meeting.

in spite of our Exisiting Auditor can other auditor filled our form Eg : DPT-3 etc

??

As per provisions of Deposit Rules, Every Company shall file a return with Registrar in FORM DPT-3 on or before the 30th day of June of every year.

Hence, the liability of filing is on the Company (No external professional certification is required) and its discretion of the Company whether it wants to file the form on its own or through any other professional.

If during February 2020, the PUC of a private limited company increased beyond 50 cr., then do we need to change the auditor who was serving for 15 years, during Feb itself or it is to be done in the ensuing AGM only.

Pursuant to the provisions of section 139 (2) of the Companies Act, read with rule 5 and 6 of the Companies (Audit & Auditors) Rules, 2014, where a private company has paid up share capital of INR 50 Crore or more, then it can’t appoint or reappoint an individual or an audit firm for more than one or two terms of consecutive 5 years respectively.

Since your company has increased the Paid up share capital of INR 50 Crore in February 2020, the company may appoint a new auditor in its ensuing General Meeting considering that there is no specific time limit stipulated in the Act for the appointment of a new auditor where the company has exceeded such threshold limit.

XYZ Company incorporated on 26.06.2019, It has appoint first auditor within 30 days from incorporation, now company wants to appoint a new auditor for signing of its first time financial statement, now question is whether company has to file ADT-1 for New Appointment and old auditor need to file ADT-03

As per provision of section 139(6) of the Companies Act, 2013, the First Auditor Appointed shall hold the office till the conclusion of the First Annual General Meeting of the Company. Thus, the first auditor shall sign the financial statements for first financial year of the Company. If the Company wants to replace the auditor, it has to follow the provisions of Section 140 for removal of auditor. There is no requirement to file ADT-3, if the first auditor has completed term as Form ADT-3 is required only in case of resignation from the office of the Auditor before the expiry of his term.

Further as per provision of Section 139(1), the Company is required to file Form ADT-1 within 15 days of the meeting in which the Auditor is appointed. Thus the Company is required to file Form ADT-1 for New Appointment.

AB Pvt. Ltd appointed an auditor for five years under Sec.139 (1) for five years in Sept. 2019 AGM. Now the company wants to change the auditor and he will resign on the date of AGM in Sept. 2020. Can the Board recommend new auditor to be held in end of Aug. 2020 for appointment in Sept. 2020 AGM. Pl let me know the procedure to be followed including the date of resignation of the existing auditor.

In case you want the new auditor to commence tenure from date of ensuing AGM, then the Board can pass a resolution proposing the appointment of the new auditor in the meeting in which the Board shall be approving the Notice of the AGM. Then, the business for appointment of auditor can be taken as ordinary business in upcoming AGM.

However, note that the resignation letter from the auditor should be received before the board meeting; only then the board can take up the matter of appointment of auditor in the board meeting.

Mr. A (CA) is appointed as first auditor of the private company within 30 days of incorporation and after few days Mr. A merge with Mr. B and enters into partnership firm. Now we have to appoint partnership firm as auditor instead of Mr. A.

Should we file Adt-3 for casual vacancy and then again file Adt-1 for appointment of partnership firm ?

There are no specific provisions under the Companies Act, 2013 on this particular matter. In case of rotation of auditors, the incoming auditor or audit firm shall not be eligible if such auditor or audit firm is associated with the outgoing auditor or audit firm under the same network of audit firms. Yes, an ADT-3 for resignation can be filed and ADT-1 can be filed with Board resolution and approval of members. Per Section 139(8) the tenure of the auditor filing the casual vacancy shall be till the conclusion of the next annual general meeting.

Hello sir, our company has appoint a auditor firm in 2004 and it continue to act as auditor till now, in the coming agm it’s tenure will be end as it was reappointed in 2015. Our company is a private company and does not come under threshold limit of 139(2). Can we again re appoint the same auditor firm for further five year.

I tried to fill ADT 1 and mention previous tenure of 15 years but it give me option of only 10 years.

Since your company does not fall under the threshold limit prescribed under Section 139(2) of the Companies, 2013, your Company is eligible to appoint the same auditor firm for a further period of 5 years. Though you are facing an error while filing the Form ADT-1, you can try the following:

• Make sure that you have entered the correct details in Form ADT-1

• Download a new form and see if the error persists

• If the error is persisting, you can raise a ticket with MCA

• Also, check if the Company is still not covered under the threshold limit

Appointment of Stat Auditor-

In a listed company, if a firm is appointed as stat auditor for a period of 5 years & dont wish to appoint it for further 5 years, is there any requirement of special notice ?

No, if the term of the auditor is expired special notice is not required to be given.

However, in case the Company is desirous of removing the auditor prior to completion of the first tenure, then, the conditions under Section 140 (including CG Approval and special notice) to be complied.

A Pvt Ltd Company appointed an auditor for 5 years. However right after signing the Financial Statements for the 2nd year , the auditor resigned 10 days before AGM. Shall it amount to casual Vacancy? can the company appoint new auditor for a period of 5 years in the AGM?

A casual vacancy in the office of auditor arisen as a result of resignation of previous auditor (any number of days prior to completion of his office tenure) is to be filed by the Board within 30 days i.e a Board Resolution to be passed to recommend to shareholders the appointment of new auditor. Thereafter a general meeting to be held within 3 months of recommendation of board to approve such appointment. Hence in your case, a Board Meeting can be conducted before the ensuing AGM and the agenda to appoint new auditor can be taken up at the ensuing AGM.

Hello sir, I’m a student, I have a query:-

ABC PUB. LTD., to which the provisions of rotation of auditor are applicable, appoints a firm as its auditor. If the audit firm resigns/ is disqualified/ is removed or due to any other reason no more the auditor of the said firm before the completion of its term (say after 2 yrs of appointment), can it be reappointed as auditor of the same firm after a period of 1yr from removal/disqualification/resignation etc. for a term of 5 yrs? If yes, Is this a loop hole in law(I dont have enough knowledge, just out of curiosity). Can the auditor be removed after every 4 years and reappointed as new auditor from sixth year for another term of 5 yrs?

The Act provides an upper cap in the number of years for which an audit firm can be appointed. Thus, even though an audit firm is appointed for a term less than 5 years or removed/ resigned/disqualified before expiry of its period of appointment, it shall be considered as one term of appointment and the auditor shall follow the provision of cooling period after it completed a period of two terms of five consecutive years.

Dear Sir,

As per section 139(2) of the Companies Act, 2013 and Rule 5 of the Companies (Audit and Auditors) Rules,2014, Listed company or a company belongs to such class or classes of companies as prescribed, one of them is (any company having public borrowings from financial institutions, banks or public deposits of rupees fifty crores or more) cannot appoint or re-appoint an audit firm as auditor for more than two terms of five consecutive years

Since the company is covered under the criteria on f.y. 2018-2019, Thus the company cannot Appoint or Reappoint an audit firm as auditor for more than two terms of five consecutive years from the f.y. 2019-2020 onwards.

Further the section 139(2) is applicable when the company belongs to such class of companies as prescribed in rule 5, so the term is counted form the appointment or reappointment after such company belongs to class of companies as prescribed i.e., in your case from the f.y. 2019-2020 onwards.

Hi Sir,

I have a question about your reply that “What will be the tenure of the new auditor being appointed in the AGM? Will it be 1 year as the auditor appointed in casual vacancy holds office upto the next AGM or will it be 5 years as the auditor is itself getting appointed in AGM and the appointment will not be treated as a casual vacancy appointment?”

Dear Reader,

Casual vacancy due to death – Board will appoint new auditor within 30 days and the auditor shall hold the office till the conclusion of AGM.

Casual vacancy due to resignation – Board will appoint the auditor within 30 days but this decision needs to be ratified by the members within 3 months and the auditor shall hold the office till the conclusion of the AGM.

Point to be noted here is that even if the members have ratified the appointment of new auditor (u/s 139(8)), the tenure is till the next AGM only. Per our understanding this is primarily to match the tenure as stated in 139 (1), i.e. tenure shall be counted from AGM to AGM. If the auditor is being appointed in the AGM, the tenure shall be 5 years as even if the auditor might have been appointed in the month of August and AGM is scheduled on 30 September, his one tenure up to the AGM is over and the nest appointment shall be for 5 years.

Sir, i have filed form RD1 along with ADT-2 and fees to RD on 04/06/2020 for removal of Auditor of a very small pvt. ltd. co. After more than a month status of SRN shows ” Pending for ROC report” . What it means and what happen next to get the approval . Is there any hearing at RD office we have to face? Pls, advise.

From your query, we could not understand which form (ADT-2 or RD-1) is having such status as ‘Pending for ROC report’. However, in our experience, for almost all e-forms requiring an RD Approval, an original hard copy of all the related documents is submitted with the RD office and thereafter a hearing is held with RD to proceed with approval of form if application is in order.

ABC Pvt Ltd has a public deposits are more than 50cr, it has appointed an individual auditor and the concept of rotation of auditor is applicable.

Now for FY 19-20 the term of 5yrs is completed but the public deposits are less than 50cr..

Is ABC pvt ltd should appoint another auditor for FY 20-21 or can continue the existing auditor as the rotations conditions are not satisfied?

Kindly please answer this… thank you in advance

Dear Sir,

Pursuant to Section 139(2)(i) of the Companies Act, 2013, after completion of term of 5 consecutive years an individual auditor cannot be re-appointed as auditor of the same company for a period of 5 years.

In the given case, since the auditor liable to rotation has completed his term of 5 years in FY 2019-20, he can be re-appointed in the same company only after FY 2024-25.

Thus, another auditor is to be appointed by the company, however, his office would be liable for rotation only when such company falls under the category of specified class of companies (http://ebook.mca.gov.in/Actpagedisplay.aspx?PAGENAME=18069).

Dear Sir

Hope you are doing well.

Please share your view in case where a private company is under the process of strike off, Do it still require to comply with the various provisions of Companies Act, 2013 viz. auditor appointment etc.

Thanks in appreciation.

As per the provisions of Section 248 of the Companies Act, 2013 and Rules made thereunder, the company shall stand dissolved on the date of publication of form STK-7 in the Official Gazette by the registrar. Therefore, until and unless the Company is dissolved all the provisions of the Companies Act, 2013 shall remain applicable to the Company.

Respected sir,

I have ABC Pvt Ltd, my auditor filed Adt-1 in 2018 till 1st AGM of 2019. subsequently he didn’t made any financial statement for 1st AGM. Now company is in default of filing and want to take a benefit of company fresh start scheme and want to file previous years filing. How I make financial statement for 2019 AGM as my auditor not taking such steps.

As we understand, the first auditor of the Company, who held office till 1st AGM, did not provide the audited financial statements for FY ended 31st March, 2019. However, the audited financials are mandatorily required to be placed in the AGM of the Company and the same is to be approved by the shareholders before filing it with the RoC. If the financials were not placed in the AGM, it is a contravention of section 129(2) of the Companies Act, 2013, and you are required to go for compounding of this offence as per section 129(7). Further, non-filing of financials is a contravention of section 137 of the Act. While delayed filing (here, under section 137) is covered under Companies Fresh Start Scheme (CFSS), the violation of law under section 129(2) is beyond its scope.

For detailed understanding, you are requested to seek professional guidance in this matter.

Respected Sir, in case of casual vacancy after appointment us 139(8) why one more ADT-1 is not required to be filed after EGM or AGM, as ultimately the appointment power of auditors rests with the Members. Or single ADT-1 could be filed after Members appointment at EGM or AGM.

Dear Sir,

The casual vacancy in the office of the auditor is required to be filed by the Board of Directors of the Company within 30 days. However, if the same has arisen due to the resignation of the previous auditor, the appointment of the new auditor shall be subject to the approval of members of the Company.

The requirement to file Form ADT-1 shall arise from:

• In case of resignation: within 15 days from the date of approval of the appointment by the members in the general meeting;

• Other than resignation: within 15 days from the date of appointment by the Board

Therefore, Form ADT-1 is filed only once after the appointment of the new auditor as per the above timeline.

The auditor is appointed in the 1st AGM, and the provisions of sec 139(2) where applicable to the company, the auditors term for 5 consecutive years are done, can that same auditor be re-appointed in 6th AGM , if provisions of sec 139(2) are not applicable to the company?

If section 139(2) of the Companies Act, 2013 is not applicable to the Company, the same auditor may be reappointed in 6th AGM of the Company.

In our case, there are three companies not falling under Sec 139(2) and where the auditor is appointed till the ensuing AGM. Here, the company does not want to re-appoint the auditors in the ensuing AGM and wants to appoint a new auditor.

1. How do we consider a term for the auditor? On the basis of F.Y. or AGM to AGM as one term?

2. Can we appoint a new auditor without the requirement of special notice under Sec 140(4)?

3. If the term will expire in the ensuing AGM then what is the process to appoint a new auditor?

4. Can the new auditor be directly appointed for a period of 5 years in the AGM after Board’s approval?

1. As per Section 139(1), the auditor shall hold office from the conclusion of the first Annual General Meeting till the conclusion of every sixth Annual General Meeting. Hence, one term shall be considered from AGM to AGM.

2. Yes, but only if the auditor has completed his tenure of five years or ten years, as the case maybe. Otherwise, if your company is replacing or appointing a new auditor in place of a retiring auditor, then your company shall mandatorily comply with section 140(4) Special Notice. However, if the auditor resigns before the expiry of his term, there will be no requirement of Special Notice.

3. Kindly refer section 139 of Companies Act, 2013 read with rule 3 of Companies (Audit & Auditors) Rules, 2014, for the process of appointment.

4. As per Section 139(1) read with Rule 3(7) of Companies (Audit & Auditors) Rules, 2014, every auditor shall be appointed for five years after the recommendation by Board/Audit Committee, if any, and approved by shareholders in Annual General Meeting.

Sir I have appointed a Auditor Firm in Causal Vacancy in May 2019 upto the Coming AGM and in that same AGM I have appointed a same auditor for 5 Years. Now in the year 2020 that Auditor Firm demerged into Proprietor. Now my question is that:

1. Whether we can appoint that same auditor.?

2. When to appoint that Same auditor and how to appoint…?

One more question is that if a tenure of auditor for appointment as an Auditor of 5 years is completed. Can he still be reappointed after 5 years or he can never be appointed in the same company. Thanks in Advance.

Your company originally appointed an Audit firm as its auditor for 5 years, which subsequently demerged into a sole proprietorship. A proprietor is considered as an individual and Rule 6(3) of Companies (Audit and Auditor) Rules, 2014, is applicable only in case of expiry of the term of the auditors.

Since this is a case of casual vacancy, your company could appoint the same auditor for a single term of 5 years. It being a casual vacancy, the Board can appoint the auditor within 30 days and no need of shareholders’ approval. Further, where an auditor completes his single tenure of 5 years or an audit firm complete its two terms of 5 years, both can be appointed in the same company only after a cooling period/ gap of further 5 years.

Previous Statutory auditor has resigned in September, 2014 and I have appointed ABC & Co. (Firm) as a Statutory Auditor for the F.Y 2014-15 by the Board of Director (No casual Vacancy arised in that year and Company incorporated in the year 2006 ). After that the Same Auditor ( ABC & Co) has been reappointed for 5 years in the Annual General Meeting on 30th Sept 2015 (from 2015-2020). Now I have following queries:

1. whether the same auditor firm can be reappointed?? if so appointed what would be the term of auditor ( whether 4 or 5 years) . if not eligible for appointed , then why?

2. 1st year of Auditor appointment can be counted as one term or not?

please clarify

The concept for rotation of auditors was introduced under the Companies Act, 2013 for specific companies as mentioned in the Act. As per the provision of Section 139(2) of the Act, those companies cannot appoint or re-appoint:

(a) an individual as an auditor for more than one term of five consecutive years; and

(b) an audit firm as auditor for more than two terms of five consecutive years:

The Companies were allowed a time period of 3 years from the date of commencement of Act i.e. 1st April, 2014 to comply with the said provision.

However, the period of auditor for which the individual or the firm has held office as auditor prior to the commencement of the Act shall be taken into account for calculating the period of five consecutive years or ten consecutive years, as the case may be.

Therefore, the re-appointment of auditor in AGM held on 30th September, 2015 for 5 years shall be counted as one term and the appointment of auditor for one term of FY 2014-15 may not be considered as one term if the appointment was due to casual vacancy. Hence, ABC & Co. may be re-appointed for one more term of 5 years.

However, if the appointment of the auditor for one financial year 2014-15 was not due to casual vacancy, such period shall be considered for calculating period of 5 years and thus ABC& Co. may be re-appointed for a period of 4 years.

Hiiiii,

Can a Company has more than one auditor for same period ????

Can auditor audit the financial statement of the financial year in which he was not auditor of that company ?

As per section 139(3)(b) and rule 6(4) of the Companies (Audit and Auditors) Rules, 2014, it can be construed that the Company can appoint two or more individuals or firms as joint auditor to whom provisions of Rotation of Auditors are applicable.

Further Section 143(2) of the Companies Act, 2014 stipulates that “the auditor shall make a report to the members of the company on the accounts examined by him and on every financial statements which are required by or under this Act to be laid before the company in general meeting…”

The auditor here means the Auditor Appointed under section 139(1) of the Companies Act, 2013. Therefore the auditor cannot audit the financial statement for the F.Y. in which he was not the auditor of that Company.

If a Company wants to appoint joint auditors in EGM for FY 2020-21 then what will be the term of the joint auditor?

Pursuant to the provisions of Section 139 of the Companies Act, 2013, every auditor shall be appointed in the Annual General Meeting by the members. Therefore, where any auditor is appointed other than the annual general meeting then the tenure shall be from the date of EGM till the date of next AGM.

However, please note that, assuming that you are appointing the auditors in EGM due to any casual vacancy in the office of previous auditor, therefore, pursuant to Section 139(8) any casual vacancy shall be filled by the Board within 30 days, but if such casual vacancy is as a result of the resignation of an auditor, such appointment shall also be approved in the general meeting convened within three months of the recommendation of the Board and he shall hold the office till the conclusion of the next annual general meeting.

In case where the company has appointed two or more joint auditors (whether individuals or firms or any other combination), the rotation may be followed in such a manner that all joint auditors do not complete their term in the same year.

ABC Pvt Ltd incorporated in Sep 2010 and appointed XYZ & Co., as their auditors. Till date (31st March 2020) they continue to be the auditors. The Company’s borrowings from Banks/ FIs exceeded Rs. 50 Crores as at March 31, 2019. Now when is the auditor liable to retire by rotation (assuming that the paid up capital has not exceeded the limits prescribed)?

Please clarify

Pursuant to the provision of section 139(2) of the Companies Act, 2013 read with Rule 5 of the Companies (Audit and Auditors) Rule, 2014, no listed company or a company belonging to such class or classes of companies as may be prescribed, shall appoint or re-appoint:

(a) an individual as auditor for more than one term of five consecutive years; and

(b) an audit firm as auditor for more than two terms of five consecutive years.

In the present case, the said provision gets attracted w.e.f. 31st March, 2019. Therefore, the term of the existing Statutory Auditor, for the purpose of rotation, shall be counted from FY 2018-19. Per this, it has completed two consecutive years as auditor and 3 years are still to be completed to constitute one term.

Could it would be possible to appoint same auditor which is appointed by board within 30 days of incorporation in first agm for the tenure of 5 year.

Yes, there is no such prohibition in the Companies Act, 2013 to appoint the same auditor if the appointment of such auditor is approved by the shareholders in the annual general meeting of the company.

sir, I have appointed ABC & Co. as a Statutory Auditor for the F.Y 2014-15 by the Board of Director due to causual Vacancy. Afterthat the Same Auditor ( ABC & Co) has been reappointed for 5 years in the Annual General Meeting on 30th Sept 2015. Now I have following queries:

1. whether the same auditor firm can be reappointed?? if so appointed what would be the term of auditor ( whether 4 or 5 years) . if not eligible for appointed , then why?

2. from last five years ( including casual vacany, the same parter has been signing the balance sheet. now whether same auditor of the ABC & co can sign the further balance sheet of upcoming 5 years or not?

The tenure of the auditor appointed in case of casual vacancy is upto the date of ensuing annual general meeting of the Company as he is appointed in the place of resigning auditor to fill the vacancy. Therefore, he can be appointed for 2 consecutive terms. Further, as per the 139 (2), one term is of 5 consecutive Years. So, the term of appointment would be 5 Years.

The same partner can further sign the balance sheet for next 5 years as there is no provision in the law about signing of balance sheet by auditors.

Director of x company resign from the office on 1-2-2018. can x company appoint him as a director of that company?

To answer this query we would need to look into what the previous designation was, terms of appointment/ re appointment, provisions of the Articles of Association and provisions of the Companies Act, 2013 based on the designation.

Can separate appointment of auditor for 1 year than 2 year after that again for 2 years consider as separate term?

“Assuming your company doesn’t fall under Section 139(2) of the Companies Act, 2013 read with Rule 5 of the Companies (Audit and Auditors) Rules, 2014.

A statutory auditor cannot be appointed for a term of less than five years, if so then the term of his/her appointment will be counted as one term. Therefore in your case the term will be counted as 3 separate term. “