An idea doesn’t become a business without effort! Budding entrepreneurs understand the effort necessary to create a business, however, they might not be familiar with the micro details of launching and running a business venture in India. You can visit our blog on Incorporating an Indian Business Entity to understand the suggested structure suitable to your business model for your intended business.

In this article, we are restricting our discussions to the most popular form of business in India: Private Limited Company. Let’s find out why!

Incorporation of a private limited company is the easiest, fastest with well-defined laws in place and is the most commonly used entry structure by foreign nationals and foreign companies. 100% Foreign Direct Investment (FDI) is allowed under the automatic route i.e no Central Government approval is required in almost all the sectors. Hence, incorporation of a private limited company as a wholly owned subsidiary of a foreign company or joint venture is the most convenient and fastest entry strategy.

FDI in almost all sectors (more than 90% of them) are under 100% automatic route barring some sectors where Government approval is required. Automatic Route is the entry route through which investment by a person resident outside India does not require the prior Reserve Bank approval or Government approval. Only such activities, which are covered under Automatic Route (and are not specifically prohibited), can be carried without obtaining RBI Approval. You can learn more about the industry specific limits and get answers to some common questions related to FDI before making your investment decision.

A recent notification , dated 17.04.2020, from the Dept. of Promotion of Industry & Internal Trade has restricted the FDI norms for neighbouring countries such as Pakistan, Bangladesh, China, etc. Investments from neighbouring countries, even those under automatic routes, shall require Government Approval.

Once a company is incorporated in India whether by Residents or by Non-Residents, be it subsidiary or wholly owned subsidiary of a foreign Company, all are treated at par with domestic companies as far as Companies Act, Income Tax, Goods and Services Tax (GST), Labour Laws etc. are concerned.

All foreign investments are repatriable (net of applicable taxes) except in cases where the investment is made or held on non-repatriation basis (done by some NRIs) at the time of investment. The common methods used for repatriation of profits are Repatriation through Dividends, Repatriation through buyback of shares or sale of shares. Proceeds are freely repatriable net of taxes.

Investment on repatriation basis means an investment, the sale/ maturity proceeds of which are (net of taxes) eligible to be repatriated out of India. The expression investment on non-repatriation basis may be construed accordingly.

Investments made on non-repatriable basis are treated as domestic investments and therefore, FDI related laws are not applicable. Generally, many Non-resident Indians (NRI’s) opt for investing on non-repatriable basis because of continued business interests in India.

| Legal Objective: |

The object and purpose of establishing must be legal and admissible in India. |

| Name: |

Unique name with words/ intent not prohibited by the Indian Government. The name of Private Company must end with the words ‘Private Limited’. |

| Directors: |

Minimum 2 Directors, 1 being a resident director i.e a director who stays in India for a total period of not less than 182 days during the financial year. |

| Shareholders: |

Minimum 2 Shareholders, whether Body Corporates or Individuals or combination of both. Note 1: The same individual can be the Director as well as the Shareholder of the Company. Note 2: The Holding Company can invest in majority shares in its own name and minority shares (even just one share) can be allotted to its nominee shareholder. Nominee shareholder is the one to whom the majority shareholder of the Company nominates to hold shares in the Company on its behalf. This can be an individual or a corporate shareholder. |

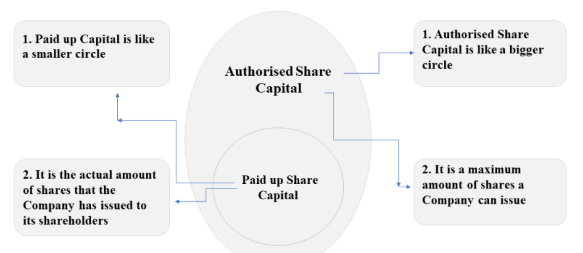

| Capital: |

The amount equivalent to paid up capital of the proposed Company should be paid within 180 days of incorporation. |

| Registered Office: |

The place of Registered Office (R.O.) of the Company should be decided considering various factors such as specific state taxes, ease of business, availability of resources, etc. In case of legal disputes, the jurisdiction of the court is determined by the location of the registered office of the company. This, therefore becomes an important factor to be considered before incorporation. Shifting of registered office from one state to another is allowed but it takes about three to four months. Irrespective of the location of the registered office, a company can do business throughout India. However, the overall legal provisions and regulations are generally common to all the states. The R.O. must be finalised within 30 days of incorporation if not at the time of incorporation. |

| Statutory Auditors: |

Companies Act mandates annual audits of the company. Such audits are performed by qualified Chartered Accountants who are external and independent parties. The first Statutory Auditor must be appointed within 30 days of incorporation. |

| Bank Account: |

One of the first steps undertaken after incorporating a private limited company is opening of the current account in the name of the Company. Now, the first bank account of the company can be opened at the time of incorporation itself, through SPICE+. |

The Government of India has integrated the process of incorporation (through Form SPICE+ ) which facilitates many other registrations covering Income Tax, GST, social laws and even opening a bank account.

The registration fees of a Private Company in India are very nominal. For Companies incorporated with Authorised Share Capital of not exceeding INR 15,00,000/- (approx. USD 19900), it does not attract any registration fees, though a nominal amount towards stamp duty is payable on the incorporation. Stamp Duty is a state subject, the state in which you propose to situate the Registered Office of the Company.

The integrated process of registration (through SPICE+) offers certain mandatory registrations along with the mandatory bank account opening at the time of incorporation.

Registration of Company does not mean immediate commencement of business. A company can commence its business/operations only after it files a declaration in Form No INC-20A declaring its registered address and with a Bank Statement showing deposit of capital by the shareholders. The INC 20A must be filed within 180 days of the Incorporation of the Company. Before the declaration in Form, INC-20A is filed by the company, the entire subscribed share capital as shown in the MOA of the company must be deposited in the bank account of the newly registered company.

Businesses should be legally compliant in order to be long term businesses. The Government of India offers various relaxations/ exemptions to private companies. However, there are some director specific or company specific compliances or event-based compliances which are to be complied by all companies as and when attracted. After the immediate post incorporation compliances , a Private Company can conduct business with minimum compliances such as the following:

|

Minimum 4 Board Meetings in a calendar year with a maximum gap of 120 days between two consecutive meetings. |

One Annual General Meeting of shareholders within prescribed timelines from closure of each financial year. |

|

You as a director can attend these meetings in person or through audio-visual means. |

You as a shareholder can attend these either in person or a proxy or an authorised representative, in case of body corporate shareholders. |

Private Company can be converted into Public Company upon approval of shareholders and the Central Government.

Private Company can also be converted into Limited Liability Partnership if it fulfils criteria under LLP Act and obtains shareholders’ approval.

Private Company can be converted into One- Person Company (OPC) falling under prescribed criteria, thresholds and upon approval of shareholders, creditors and ROC. It is prudent to note that as on date of submission of application for such conversion, there must not be any foreign shareholding in the Company i.e all the shares must be held by a natural person who is a Citizen and Resident in India.

Closure of a company has been simplified and streamlined matching the international standards with the notification of Insolvency and Bankruptcy Code (IBC) in 2016. Closure, initiated by the company, can primarily be in two ways: Strike Off or Voluntary Liquidation. In case you do not wish to permanently close down the business and want to wait for the right time, you can also seek status of ‘Dormant Company’.