State Governments levy and collect stamp duty on issue of Share Certificates which fall within the sphere of State Legislature by virtue of the powers given to the State Governments through our Constitution (Entry 63 in the State List). Through this article, we would like to cover the Stamp Duty paid by the Companies incorporated in the National Capital Territory of Delhi. Companies need to pay Stamp duty on the occurrence of below mentioned events:

| Particulars | Amount of Stamp Duty Applicable (NCT of Delhi) | |

| In respect of a company having share capital | Stamp Duty for Spice form is INR 10/- | |

| MOA | INR 200/- | |

| AOA | 0.15% of Authorized Share Capital | |

LEGAL ASPECTS

Companies Act, 2013: As per the provisions of the Companies Act, 2013, the Share Certificate should be issued within two months from the date of incorporation or from the date of allotment, as the case maybe {Pursuant to Section 56, 403 read with Rule 12 of Companies (Registration of Offices and Fees) Rules, 2014}.

Indian Stamp Act, 1899: The legal provisions for payment of Stamp Duty is covered under section 3 and 10 of the Indian Stamp Act, 1899 and the time limit of one month after execution of instruments for payment of stamp duty is covered under first proviso of section 32 of the Act.

PROCEDURE FOR MAKING THE PAYMENT OF STAMP DUTY IN NCT OF DELHI

CONSEQUENCES OF DELAY IN PAYMENT OF STAMP DUTY ON ISSUE OF SHARE CERTIFICATES

Where any delay happens in making the payment of Stamp Duty, the Company shall be liable for penalty under the Indian Stamp Act, 1899. The Authority has the discretion of imposing a penalty upto 10 times of duty amount payable (see proviso of section 35 of the Indian Stamp Act, 1899).

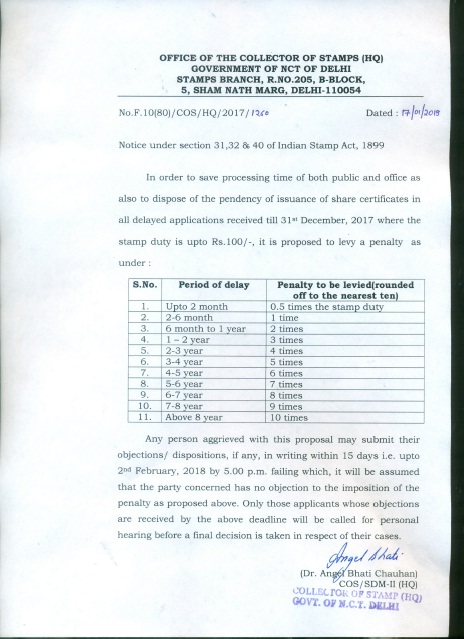

RECENT AMENDMENT IN CASE OF DELAYED APPLICATION FOR STAMP DUTY

In the event of delay, the whole procedure of getting share certificates stamped takes time. To save processing time, one of the recent steps proposed by Collector of Stamps, Govt. of Delhi (vide NO.F.10(80)/COS/HQ/2017/1260) was providing conclusive figures of penalty to be levied based on period of delay caused instead of levying penalty arbitrarily and the amount of penalty ranged from 0.5 times of stamp duty amount for delay upto 2 months to 10 times of stamp duty for delays beyond 8 years. The above notification was issued to dispose of the delayed cases of payment of stamp duty on issuance of share certificates where the application was made to SHCIL upto 31st December, 2017 and the stamp duty amount was upto INR 100/-. Any person who had any objection was given an opportunity to submit his objections till 2nd February, 2018.

The above decision of the Ministry was welcomed with a positive response from the Industry as it provided lot of convenience. We appreciate such proactive approach by the Government and in our opinion, such orders should find a permanent place in their rule book. Further, it should also be extended to some higher nominal benchmark which is commensurate with the present times. This will smoothen the entire process and provide for speedy disposal of delayed cases.

{kind=link}

what is stamp duty rate on share subscription agreement and share holder agreement in delhi?

Dear Reader,

A Shareholders’ Agreement is considered a general agreement as it is a contract between the shareholders of a company, which outlines the rights and obligations of each shareholder with respect to the company. The agreement sets the terms and conditions under which the shareholders will own and manage the company, and typically includes provisions related to the transfer of shares, management of the company, distribution of dividends, and other important matters.

As per Article 5 of Schedule 1A of the Indian Stamp Act, the stamp duty (in Delhi) for a Shareholders’ Agreement is charged at a flat rate of Rs 50, regardless of the value of the shares or the size of the company.

how to pay stamp duty in Maharashtra on physical allotment of shares to the another partner of the company. Reply as soon as possible

For payment of Stamp Duty, Maharashtra has made its own online portal for this purpose i.e. GRAS (Government Receipts Accounting System) Finance Department, Government of Maharashtra which can be accessed at https://gras.mahakosh.gov.in/echallan/.

You can get yourself either registered here or pay without registration. The process for payment has already been provided at the aforesaid site, you may refer to the same.

If share stamping fee is not paid at the time of share allotment when co. is incorporated( since 2013) but now, want share certificate of earlier shareholder on which stamping fees should be paid and also we have no records of earlier shareholder to whom share certificate should be issued then what is procedure for getting share certificate.

Kindly reply.

According to Section 32 of the Indian Stamp Act, 1899 every Company is required to pay Stamp Duty on the allotment of shares within 30 days from the date of issuance of Share Certificate at the rate of Rs. 1 for every Rs. 1000 or part thereof of the value of the share including the amount of premium.

However, if Company fails to pay the stamp duty within the prescribed time then according to provision 35 of the Indian Stamp Act, 1899 the Company shall be liable for a penalty which may extend to 10 times of the stamp duty or can file an application for impounding.

Since your query requires research, you are requested to seek professional advice in this matter.

A private limited is having 1,36,00,000 nos. of preference shares, now it is proposing to convert 14,00,000 nos. of the said preference shares into equity shares.

Accordingly, we need to split the old share certificate into two new certificates of 14,00,000 nos. of equity shares and remaining 1,22,00,000 of preference share.

Kindly advice do we need to pay stamp duty for both the new share certificates issued in lieu of the old share certificate?

As per the provisions of the Indian Stamp Act, 1899, stamp duty is paid at the time of issuance of shares and execution of share certificates. Merely splitting of previously issued share certificates does not attract the payment of stamp. In your case, no stamp duty is required to be paid, if paid earlier.

Very good article. Could you specify if Stamp duty is payable AGAIN on value of very first Share certificate (which is first subscribed capital at Face value at incorporation) even after – already having made once a payment through SPICE on MOA AOA of Stamp duty on subscribed capital at time of incorporation ?

The provisions of stamping are contained in the Indian Stamp Act, 1899. The Act specifies payment of stamp duty on Memorandum & Articles of association and Share Certificates separately as these are two different instruments. So, yes the stamp duty shall be paid on first Share certificate (which is first subscribed capital at Face value at incorporation) even after – already having made once a payment through SPICE on MOA AOA of Stamp duty on subscribed capital at time of incorporation.

Share issued and allotted in electronic form attracts the Stamp Duty? In case of Wholly Owned Subsidiary Unlisted Public Company

As per Section 8A of the Indian Stamp Act, 1899 the securities issued in electronic form are liable to payment of stamp duty. Hence, in respect of such issue, the shares shall be chargeable with stamp duty on the total amount of security issued and such securities need not be stamped. However, in case of transfer of shares in electronic form, the payment of stamp duty is exempt.

If a Company having registered office in MP and issuing the Share Certificates in Gujarat, then where to pay stamp duty ? to MP State or Guajarat ?

As per Section 3 of Indian Stamps Act 1899, Every Share Certificate must bear the necessary stamp duty as per the Stamp Act of the respective State/ Union Territory from which Certificate is issued.

Therefore, Stamp duty shall be payable at Gujarat.

Is stamp duty payable for issuance of shares certificate by government company to goverment of india.i.e concerned ministry. Is there is any exemption.

Proviso to Sec 3 of Indian Stamp Act, 1899 exempts government from payment of stamp duty where such government is liable to pay duty chargeable to an instrument. (modify the answer after proper discussion with others)

Proviso to Sec 3 of Indian Stamp Act, 1899 exempts government from payment of stamp duty where such government is liable to pay duty chargeable to an instrument.

Its very knowledgeable and informative article….